First party Fraud

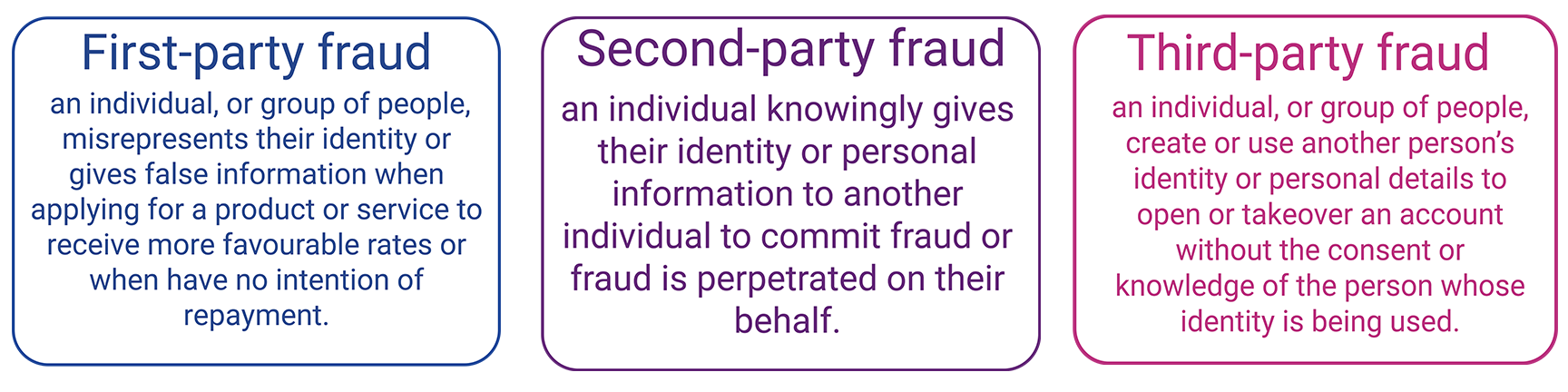

First party fraud is where an individual, or group of people, misrepresent their identity or give false information. This is usually done when applying for a product or service to receive more favourable rates, or if they have no intention of meeting their commitments. Another example could be if an individual can make a false claim against an insurer to obtain a payment they are not eligible for.

“People are being dishonest to get a mortgage they might not otherwise be eligible for.”

Our analysis shows how more people are committing fraud. People are being dishonest to get a mortgage they might not otherwise be eligible for, by not being truthful about their employment or financial circumstances. Within insurance, we see people manipulating their details on a policy to get a better premium, from advising where a car is parked to intentionally adjusting policies mid-term.

Another interesting trend is that during major events there tends to be a short-term increase in first party fraud cases detected. For example, during the World Cup, someone will go and buy a flat screen television on credit and, following this, they’ll get a call from their provider asking if they had brought the TV as it’s an unusual purchase. The individual then might deny buying the TV and will get a refund from their card provider. When customers dispute legitimate purchases to receive a refund from the issuing bank, this is also known as friendly fraud or charge back fraud.

Second party fraud

Second party fraud, or money mules, is where an individual knowingly gives their identity or personal information to another individual to commit fraud.

Businesses can find second party fraud difficult to detect and challenge as the person who’s identity being used to commit fraud, has knowingly allowed it to take place. This means the usual traces or behavioural characteristics associated with fraud aren’t so overt and are harder to spot.

“Businesses can find second party fraud difficult to detect and challenge.”

The individual may refuse to acknowledge they were involved or don’t report what’s happened, making it difficult for businesses to prove the individual was involved without firm evidence. This fraud could occur as an individual is going through financial difficulty, or as a means to fast cash. Examples include signs in supermarkets or a shop saying such things as ‘do you want to earn £200 fast?’ which could be inviting for cash-strapped or vulnerable individuals. Their details are then used to commit fraud. According to Cifas[1], the amount of 14-24 year olds being used as money mules has increased by 27% during 2017.

Third party Fraud

Third party fraud is where an individual, or group of people, use another person’s identity or personal details to open or takeover an account without the consent, or knowledge, of the person whose identity is being used. Another form of third party fraud is manufactured identities where an individual creates a new identity from stolen and false information.

Third party fraud is a significant trend. It is also associated with organised criminal activities, with up to 50% of third party fraud seen as part of a fraud ring with frauds linked across multiple identifies. Third party fraudsters acquire personal identifiable information (a full set of PII can be available for as little as £43 on the dark web) and then use the data to take over an identity which is used to gain credit or products.

“Third party fraud is a significant trend. It is also associated with organised criminal activities.”

Young people are the most likely to be targeted and are two and a half times more likely to be a victim. Fraud in the mobile telecom market is also prevalent with people taking out a phone contract using someone else’s identity, receiving the handset and then selling it on immediately. With handsets now costing upwards of £1000 this is a profitable scam.

Find out how you can protect yourself, your business and you customers. View the reality of fraud threats Experian guide for the latest trends and vulnerabilities businesses are facing. This guide also looks at what businesses should consider to address fraud threats.

[1] https://www.cifas.org.uk/newsroom/new-data-reveals-stark-increase-young-people-acting-money-mules