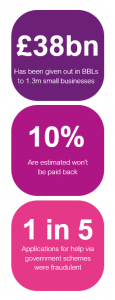

But in previous economic downturns we almost always witness and increase in corporate insolvencies and a reduction in new businesses being registered. Covid-19 has been different- insolvency rates have decreased due to government support; however, we’ve had a rise in new start-ups and business aren’t closing. The concern is that people are using BBLS inappropriately to create fraudulent businesses out of the pandemic. Businesses need to be able to ensure the business they are working with are real and the people behind the business are real and have no previous fraud issues.

But in previous economic downturns we almost always witness and increase in corporate insolvencies and a reduction in new businesses being registered. Covid-19 has been different- insolvency rates have decreased due to government support; however, we’ve had a rise in new start-ups and business aren’t closing. The concern is that people are using BBLS inappropriately to create fraudulent businesses out of the pandemic. Businesses need to be able to ensure the business they are working with are real and the people behind the business are real and have no previous fraud issues.

What types of fraud are we seeing?

Eligibility fraud– Misrepresenting credentials to receive a loan or service that they are not eligible for or increasing the amount that they can get

Business owner impersonation– Director impersonation or stealing identity of business

Habitual credit abusers– Fraudsters who understand a business’s processes for onboarding will set up and close accounts through Companies House therefore can evade paying creditors

Duplicate bounce back loans applications

Key questions to clearly identify a good business

- Can I validate the existence of the business and that the contacts presented are associated with that business?

- Am I able to confirm the identity of the key people owning or controlling the business? – understanding who the ultimate beneficial owner (UBO) is.

- Are the owners of the business connected to known frauds? -Ensuring a business if not connected to known fraudulent databases- national hunter/ CIFAS

- Are the business or owners connected to internal ‘suspect’ databases? – Checking if you have accumulated information on this business customers and identifying if the outcome has not been a favourable one

- Is the delivery address confirmed as being associated to the business?

- Can the business bank account be validated and associated with the business? This is important if you are granting a loan to ensure the account that business are paying funds into are associated with the business that is making the application.

What data can be used to establish suspicion?

All of the data is available at any time but to really see the true value it needs to be used together, bringing the data together allows you to really join the dots and use it to establish suspicion.

Internal data

- Suspect files– associated a company with suspicion therefore released a suspicious activity report to the National Crime Agency.

- Exit Lists– exited a business based on the suspecting them of fraud

- Credit abusers– People who understand your processes and have tried to take advantage of it

- Known fraudsters you have dealt with in the past.

External Business Risk Data

Experian have developed several business risk flags giving businesses deeper fraud insights.

- Suspicious Phoenix company flags– These flags have been developed using our bureau data to identify directors who are leaving a trail of debt behind them enabling you to identify these potentially suspicious businesses

- Zombie director flags– flags which identify directors who have been appointed after their death

- Stolen and duplicated accounts flags – flags which identify businesses going to Companies House and stealing the accounts of other business and passing them off as their own

- Inaccurate reporting flags – flags inaccurate turnover values presented to Companies House which have been embellished and misalign to what we are seeing in the bureau.

External Consumer Risk Data

Experian have access to several external fraud databases that have developed their own risk flags

- Access to National Hunter

- CIFAS

- Mortality Data

- Never Paid Defaults (a first party fraud indicator)

- High risk multi-occupancy addresses

Connecting businesses to known frauds associated with the business or its owners

The diagram shows the corporate structure of a business can be complex. Some businesses have parent companies, ultimate parent companies and subsidies. Businesses need to understand if a business has parent companies etc and how are they linked together and understand whether the UBOs, directors or shareholders are connected to known fraud databases.

The director in most business will have a public service address and is most commonly a company address which means the address will not match in our consumer databases or external consumer databases. Experian have unique access to Usual Residential Address (URA) data. This enables Experian to leverage the Directors full residential address and Date of Birth to authenticate key parties and match them against Fraud databases.

We bring together the breadth of Experian data from consumer, commercial, identity and fraud with your own data to create tangible data insights to allow you to authenticate a business, its owners and accurately identify commercial fraud. We are the only provider who can arm you with business, ownership, consumer, identity and fraud data.

How do we do this?

Our new service will enable you to give us your customer file. We will cleanse, standardise and format the client input data to maximise match rates to Experian Business Bureau Data and Third-Party Data Sources.

We will then append key parties to all companies in each file, including UBO’s, PSC’s and Directors. This allows us to connect to CIFAS and National Hunter to look whether those business owner as associated or connected with known fraudsters. In parallel to this, we will run the business against our commercial authentication service which will validate that business exists and if it is actively trading

We can leverage hierarchical identifiers to link sites, subsidiaries, parents and ultimate parent companies together and Key Party identifiers to link business owners. This crucial step will expose where hidden business and key party links exist between the Suspect File and Existing Customer and Applicant files.

What value can it bring to your business?

- Flag fraudulent accounts that are in arrears

- Stop any new lending or extending new services to that business

- Focus your collections strategy

- Process high volumes of checks- designed to support automation and give you visibility and insights quickly

- Reduce Bad Debt Charge

- Reduce Fraud Losses

- Avoid reputational damage

Here at Experian, we’re committed to sharing our data and insights to help you understand the changing landscape and where your concentrations of risk are, as well as unearth new trends. We are in the unique and unrivalled position of being able to overlay economic foresight onto credit insights to get both a back and forward-looking view – and our innovation agenda is committed to developing tools which can help you and your customers thrive, even in these uncertain times. To find out more please contact us