An unprecedented cost-of-living crisis is reshaping the UK credit landscape

Its impact is being felt across all UK households, and whilst its effect may be different for individuals, its reach is all encompassing. Download our guide on navigating this new credit landscape. In this new landscape, well-worn indicators of consumer stress – such as unemployment – are no longer the best predictors of ability to pay. Instead, the focus has shifted to understanding real disposable income.

Lenders who can understand the nuances and complexity in granular detail to determine risk and spot growth opportunities will be the winners in this new landscape.

Download this whitepaper to help guide you through the new UK credit landscape.

The first signs of stress appearing

The credit market has recovered well from lockdown measures: all sectors except personal loans have recovered to pre-Covid new business volumes, and the UK economy is strong despite the ravages of the pandemic. However, we can now see the first signs of stress appearing amongst consumers.

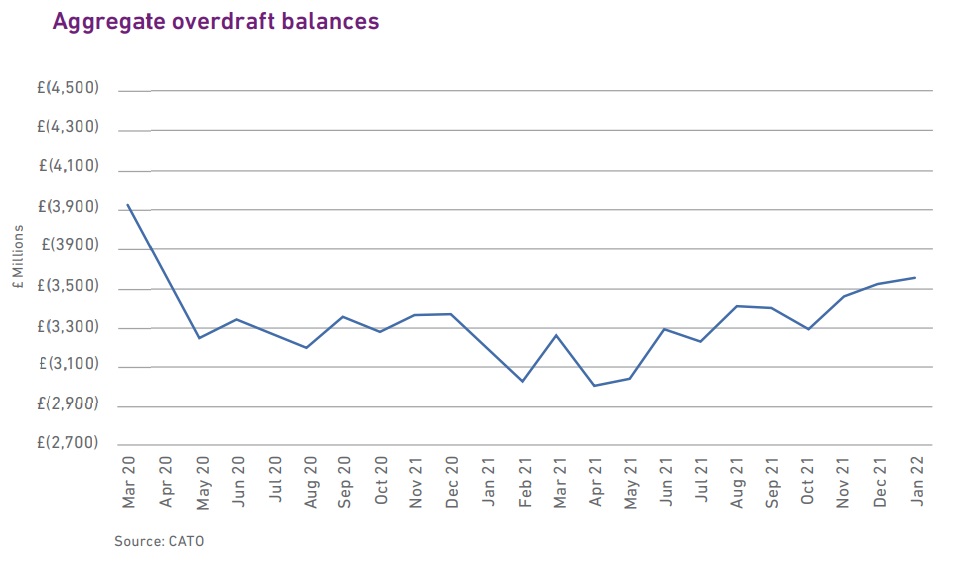

Current-account balances are falling

Credit-card balances are rising

Overdraft use is rising

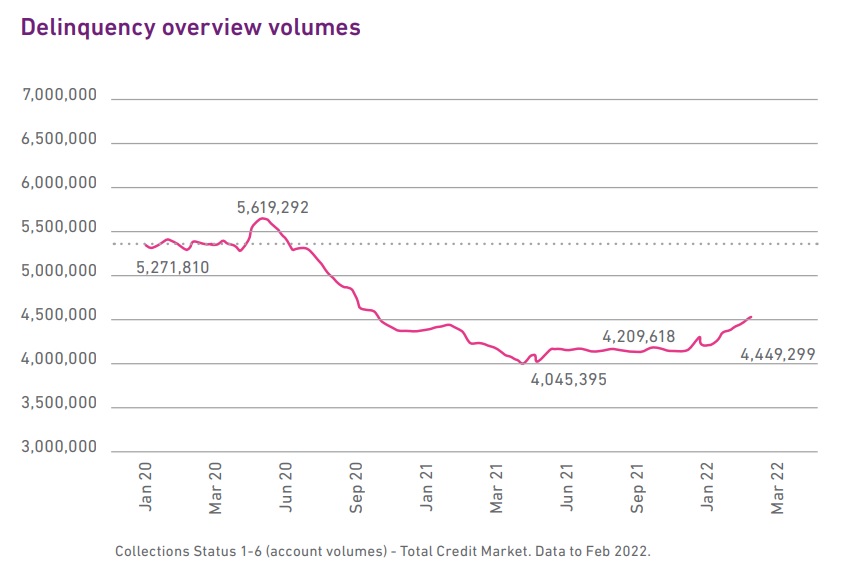

Collections cases rose 7% between December 2021 and February 2022

In this insight report we cover:

the rapid recovery of the UK economy and credit markets post pandemic

test

the evolving nature of the cost-of-living squeeze and its impact on credit markets

test

the key features of the new credit landscape

test

what this landscape looks like for consumers

test

A rapid recovery:

The UK economy and credit markets in March 2022

Strong bounce in GDP

The economy roared back into life as the lockdown eased in the summer of 2020, and it kept growing in 2021 despite a second national lockdown. It has regained its pre-Covid size. In 2021 GDP grew by 7.5% – the fastest rate in the advanced world. Growth is flattening, but Experian’s economists still predict that UK GDP will grow by another 4.7% in 2022.

Unemployment low

The UK unemployment rate is back at pre-pandemic levels. This is unexpectedly good news: early in the pandemic many predicted it would soar beyond 10%. Unemployment has in the past been a key predictor of a borrower’s likelihood of default, though this pattern is becoming significantly more complex as more people have changed jobs, switched to flexible working or opted out of full-time employment.

Credit delinquency low

The credit market has been buoyed by low levels of defaults. Strikingly, delinquency fell during the pandemic, with many consumers cutting spending, repaying debt and, in some cases, receiving government and/or lender support that enabled them to meet repayments more comfortably.

New-agreement volumes recover

New credit agreements bounced back by 8% in 2021, driven mainly by demand for credit cards. By early 2022, monthly application volumes were back at or above pre-pandemic levels in all credit markets except loans. The UK credit market has come out of the pandemic in robust shape.

Current-account balances down

The growth in current-account balances over the pandemic seems to have peaked. Aggregate balances are now slowly falling (Experian data).

Overdraft usage up

From a low base, overdraft balances are trending upwards – suggesting that more consumers are needing more leeway to meet costs (Experian data). 4.6m current accounts are in overdraft, up 17% from the low point in May 2021.

Delinquency edging upwards

The total volume of collections cases fell during the pandemic but increased by 7% between December 2021 and February 2022 (Experian data).

At the point of writing, the first signs of stress among borrowers are becoming apparent. These trends are likely to continue in the coming months as the impact of inflation, price rises and shrinking disposable income grows.

The cost-of-living crisis: Record falls in real disposable income

According to the Bank of England (BOE), real income will be squeezed harder in 2022 than at any time since the Second World War. The BOE estimates that real incomes – a measure of the actual purchasing power of what we earn – will fall by 2%.

Did you enjoy the read?

Download the full paper on navigating this new credit landscape

Discover how you can manage risk and seize opportunities during the cost-of-living squeeze and beyond.

Do your customers have the ability to pay?

Whilst credit scoring has been used successfully for many years to assess the creditworthiness of new applicants for credit it has some limitations: it has tended to focus on establishing an individual’s propensity to pay rather than their ability to pay.Consumers with a high willingness to pay may not be able to afford to buy an asset at a given price; which means that, if the source of income is not verified, ability to pay could be overlooked, resulting in the wrong decisions being made.That’s why (especially where credit bureau information is unavailable) many lenders are examining in detail their processes on income and expenditure determination and the calculation of net disposable income estimates. Their scope is to enhance the ability to pay calculation that will allow them to understand the key drivers of customer performance and to demonstrate, where required, compliance with regulators.Estimating income using advanced analytics

Understanding the true income of customers requires sophisticated solutions. By using advanced analytics you can assess a customer’s complete financial picture and improve decision making by providing in-depth insight into a customer’s overall credit capacity.The “philosophical” reasoning behind income modelling may be readily apparent – for example, a consumer whose credit history reflects a mortgage open for five years with a given payment, an instalment loan for a car with a given payment and open revolving accounts, and who has had no material delinquencies is likely to have a certain amount of income in order to support those payments.The advanced analytics approach to income estimation covers the below elements:- Definition of data layer for the identification of internal and external data sources that are relevant to observe or estimate income

- Calculation of target variable through the definition of the target variable for modelling

- Development of clusters for the creation of homogeneous groups that can be specifically used for estimating separated models

- Build of models and validation through the application of analytical techniques to obtain income estimation models and validate them on an on-going basis

- Definition of the business strategy to incorporate the income estimation into the day-to-day lender’s activities

- Monitoring of results to ensure the impact to the business is aligned with expectations

Benefits of income estimation models

Income estimation models allow – through multiple uses across the life cycle –reduced manual and expensive verification procedures, better understanding of the consumer’s ability to pay, improved underwriting processes, measurement of the customer’s potential value in the near future, and increased collections recovery by targeting the individuals most likely to be able to pay.Income estimation models also provide greater efficiencies by validating consumer income in real time, a better consumer experience by protecting consumer privacy using an alternative to consumer-stated income and cost savings by improving efficiency through time-consuming prioritisation and expensive income verification.Implementing a robust method for estimating income can help increase the security of lenders in finding the right customers and making them the right offer. A flexible, practical and compliant measure of consumer’s capacity to take on additional credit enables the achievement of financial success and business growth through enhanced customer experience. [post_title] => Income estimation at the heart of responsible lending [post_excerpt] => [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => income-estimation-at-the-heart-of-responsible-lending [to_ping] => [pinged] => [post_modified] => 2023-05-09 10:25:20 [post_modified_gmt] => 2023-05-09 09:25:20 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14508 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw ))[1] => Array ( [post] => WP_Post Object ( [ID] => 14174 [post_author] => 1 [post_date] => 2020-07-28 17:17:13 [post_date_gmt] => 2020-07-28 16:17:13 [post_content] => [post_title] => How Open Banking's arrival is removing consumer friction in credit application across Europe [post_excerpt] => [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => how-open-bankings-arrival-is-removing-consumer-friction-in-credit-application-across-europe [to_ping] => [pinged] => [post_modified] => 2020-08-26 14:42:13 [post_modified_gmt] => 2020-08-26 13:42:13 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14174 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw ))[2] => Array ( [post] => WP_Post Object ( [ID] => 14130 [post_author] => 1 [post_date] => 2020-07-28 15:50:12 [post_date_gmt] => 2020-07-28 14:50:12 [post_content] => [post_title] => Covid-19 credit activity in week 2 - how are we addressing the risk of increased fraud during this time? [post_excerpt] => In this webinar we will highlight early consumer credit trends and risks we see unfolding and explore fraudulent activities that are manifesting. [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => covid-19-credit-activity-in-week-2-how-are-we-addressing-the-risk-of-increased-fraud-during-this-time [to_ping] => [pinged] => [post_modified] => 2020-08-26 14:41:58 [post_modified_gmt] => 2020-08-26 13:41:58 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14130 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw )))

Further reading

Income estimation at the heart of responsible lending

In today’s financial market, it’s critical to have a comprehensive view of your customers’ ability to pay in both the short and longer term. Read our blog for more insight.

How Open Banking’s arrival is removing consumer friction in credit application across Europe

TBC

Covid-19 credit activity in week 2 – how are we addressing the risk of increased fraud during this time?

In week 2, we share what the credit activity looks like and how to address the risk of increased fraud. Watch our webinar.

Guide Template Test

What your business credit score means and how to improve it

How will customer behaviours change with the cost-of-living crisis?

Test Download

Download the webinar blah blah blah

How has the COVID19 crisis impacted on consumers – Experian’s Consumer Default Index

Watch our webinar we look at the new normal and consider the Consumer Default Index (CDI) results on first-time defaulted balances.

Collections during and after the pandemic

This webinar, presented in Dutch, addresses the most important aspects of collections and customer management during and after the coronavirus crisis.

Covid-19: regulatory

Le Covid-19 aura un impact économique sur toutes les économies, les chocs sur les investissements et la demande déclenchant un ralentissement qui devrait durer jusqu'à la fin du mois de juillet 2020. Cette perturbation économique et cette reprise étendue auront un impact significatif sur le secteur bancaire, avec une forte augmentation des niveaux de prêts non performants, des provisions et une pénurie de capitaux.Les flux de revenus seront modifiés rapidement et de manière significative. Il sera donc de plus en plus important pour les fournisseurs de crédit de comprendre ces changements rapides en temps réel, afin de pouvoir protéger à la fois leurs clients et leurs portefeuilles de prêtsVisionnez notre webinaire à la demande "La reprise économique et l’impact sur les réglementations" et découvrez comment Experian peut vous aider à faire face au nouvel état de notre monde. Découvrez les impacts du Covid-19 et comment améliorer les stratégies de votre entreprise tout en vous adaptant aux nouvelles réglementations.