The growth of digital has reshaped the speed at which organisations and governments adapt to identity and ledger design

ID has evolved over many centuries, with the first written identity documents — passports — being created in the 1400s. The modern version of this passport came into existence in 1914. From those early efforts, other government issued identity documents, including driver’s licences, arose. Now, digital and physical identities are linked. Licences and passports often include biometric markers, such as facial, hand or iris verification. Through this, it is possible to know exactly who is interacting with a company through their website, app, in person or on the phone.

In the years leading up to the pandemic, many organisations had been investing in digital transformation programmes, but the pandemic pushed every organisation into this space and, in 2020, anything that could be moved online was moved online. And in the midst of this upheaval, they saw seismic shifts in customer behaviour and expectations. Consumers had little choice but to turn to digital channels and services en masse during the pandemic. As digital adoption has increased, identities have become more complex.

Read our whitepaper ‘Capturing the digital identity evolution through a layered approach‘ for more insights into the future of digital identity.

While some things have changed, certain requirements remain in any identity platform design

Standardisation: An organisation needs the ability to consistently capture data and characteristics that can be useful to a specific individual. As more standards are built into the identification artifact, organisations are better able to verify identity. Interoperability: An organisation must have the ability to resolve an identity to a specific person, which could involve recognising the phone number when a customer calls a contact center, recognising the user ID and password or a device when a user logs in to an online platform, etc., and using that data to determine the user of the identity is in fact the identity owner.

Banks and financial institutions

have added digital services by incorporating electronic Know Your Customer (eKYC) in some geographies to ensure that institutions have verified the user.

eCommerce firms

have implemented authentication tools such as biometrics to verify identities for digital payments.

The National Health Service (NHS)

has incorporated verification tools while also adhering to strict privacy rules under the General Data Protection Regulation (GDPR), allowing for better care across a patient’s health team.

In this insight report we cover:

The present state of Digital Identity

Test

COVID-19’s Impact on Digital Transformation and Identity

Test

The challenges to overcome

Test

The future of Identity and constructing future Identities for Businesses and Consumers

Test

The present state of

Digital Identity

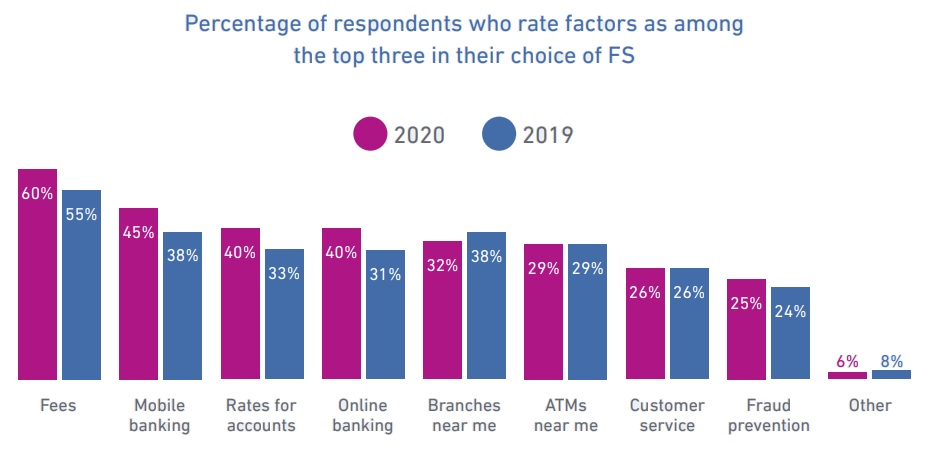

The consumer preference for digital services

One reason banks, eCommerce, and healthcare organisations have had to adjust to put digital identity at the forefront is that customers have come to require – and seek – online offerings.

Online banking, for example, increased from 37% in June 2020 to 40% in January 2021. The numbers vary depending on the age group. Consumers over 40 are more likely to use online banking – 40% compared to 36% of those under the age of 40. The use of mobile wallets is also strong. In the UK, 65% of consumers use mobile wallets – globally it’s 70% of consumers using mobile wallets.1

Mobile and online banking have become a must-have for consumers

The consumer preference for digital services goes well beyond banking to all areas of life, impacting a variety of industries. Those over the age of 40 increased their rate of online grocery shopping by 10 percentage points over the past two years.2 The same goes for online food delivery 2020 witnessed restaurant-to-consumer deliveries grow by £3.7bn to reach £11.4bn – double the 2015 market value – and that number is expected to grow to £12.6bn by 2024.

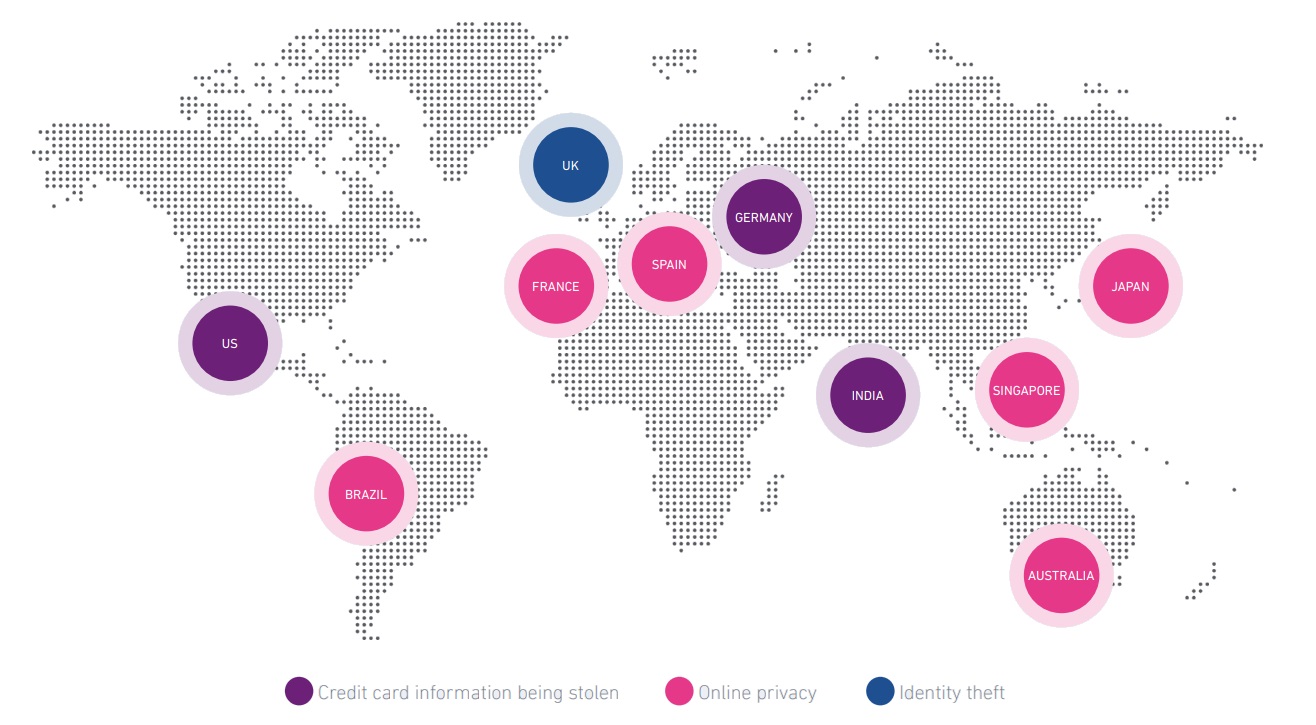

Depending on where your customers live, privacy and security concerns differ

A further dimension to consider when designing digital identity verification solutions are the many regional differences when it comes to consumer concerns. In some regions, identity theft will be the greatest area of concern, in others, privacy. These nuances need to be addressed in the required degree of friction that consumers need to experience when verifying their identities. Matching consumer concerns will be critical in how willing they are to complete certain verification activities.

Low Assurance Use Cases: In areas and sectors where reducing friction is the number one concern with onboarding, reducing the layers provides identification but eases restrictions. This occurs often in eCommerce settings, as well as social media onboarding. In such cases, the level of digital identity verification may range from single sign-on to two-factor authentication with an email or phone validation. The more assurances an organisation has of the identity – even in low assurance use cases – the better they can protect against fraud while ensuring friction remains limited.

Medium Assurance Use Cases: In situations where fraud potential may rise, privacy concerns heighten, or compliance efforts become more complicated, organisations will seek a greater level of verification. Payment processing, education, and gaming organisations may require this level of verification, which can include a proof of ID through a document. In a digital identity setting, it could require an identification document with matching biometrics.

High Assurance Use Cases: In the banking, healthcare, government and insurance sectors, among others, the need to secure the funds, pass compliance – Know Your Customer (KYC), anti-money laundering (AML) efforts – or address heightened privacy concerns becomes paramount. In such cases, flows may require multiple layers of identification, from physical IDs, to biometric identification, to validation of certain ID attributes, like a date of birth.

COVID-19’s impact on digital transformation and identity

As consumers adjusted to online offerings during the pandemic, so did companies. Eight in ten companies now have a customer recognition strategy, marking a 26% year-over-year increase.

Similar trends hold true with digital customer journey strategies, with 90% of companies having one in place at the start of 2021; 46% implemented one during the pandemic. Globally, 52% of firms expect to invest in advanced analytics or artificial intelligence (AI), which better captures the customer identity. Increasing digital operations and customer service also has high rates, with 49% of companies in India, 37% in Brazil, and 36% of Japan, Singapore and the US. While only 19% of UK businesses plan to do so.

For banks and financial technology firms, the pandemic encouraged a push towards more accessible banking offerings, which benefitted institutions that could blend the security with the ease of use. By incorporating digital identity layers within the compliance and security process, which already secures KYC and AML compliance, financial institutions and FinTechs can better provide services with reduced friction, particularly for customers that have a relatively comprehensive, low-risk identity. In such cases, the digital identity layer can allow the user to speed through new sign-ups, account access, or other services, since the organisation can trust the verification

Smll business owner sending voice message while standing by window. Entrepreneur using smart phone while looking away. He wearing apron in store.

Did you enjoy the read?

Download the full paper on capturing the digital identity evolution

Read our whitepaper ‘Capturing the digital identity evolution through a layered approach‘ for more insights into the future of digital identity.

Download the whitepaper - "Capturing the digital identity evolution through a layered approach"

Do your customers have the ability to pay?

Whilst credit scoring has been used successfully for many years to assess the creditworthiness of new applicants for credit it has some limitations: it has tended to focus on establishing an individual’s propensity to pay rather than their ability to pay.Consumers with a high willingness to pay may not be able to afford to buy an asset at a given price; which means that, if the source of income is not verified, ability to pay could be overlooked, resulting in the wrong decisions being made.That’s why (especially where credit bureau information is unavailable) many lenders are examining in detail their processes on income and expenditure determination and the calculation of net disposable income estimates. Their scope is to enhance the ability to pay calculation that will allow them to understand the key drivers of customer performance and to demonstrate, where required, compliance with regulators.Estimating income using advanced analytics

Understanding the true income of customers requires sophisticated solutions. By using advanced analytics you can assess a customer’s complete financial picture and improve decision making by providing in-depth insight into a customer’s overall credit capacity.The “philosophical” reasoning behind income modelling may be readily apparent – for example, a consumer whose credit history reflects a mortgage open for five years with a given payment, an instalment loan for a car with a given payment and open revolving accounts, and who has had no material delinquencies is likely to have a certain amount of income in order to support those payments.The advanced analytics approach to income estimation covers the below elements:- Definition of data layer for the identification of internal and external data sources that are relevant to observe or estimate income

- Calculation of target variable through the definition of the target variable for modelling

- Development of clusters for the creation of homogeneous groups that can be specifically used for estimating separated models

- Build of models and validation through the application of analytical techniques to obtain income estimation models and validate them on an on-going basis

- Definition of the business strategy to incorporate the income estimation into the day-to-day lender’s activities

- Monitoring of results to ensure the impact to the business is aligned with expectations

Benefits of income estimation models

Income estimation models allow – through multiple uses across the life cycle –reduced manual and expensive verification procedures, better understanding of the consumer’s ability to pay, improved underwriting processes, measurement of the customer’s potential value in the near future, and increased collections recovery by targeting the individuals most likely to be able to pay.Income estimation models also provide greater efficiencies by validating consumer income in real time, a better consumer experience by protecting consumer privacy using an alternative to consumer-stated income and cost savings by improving efficiency through time-consuming prioritisation and expensive income verification.Implementing a robust method for estimating income can help increase the security of lenders in finding the right customers and making them the right offer. A flexible, practical and compliant measure of consumer’s capacity to take on additional credit enables the achievement of financial success and business growth through enhanced customer experience. [post_title] => Income estimation at the heart of responsible lending [post_excerpt] => [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => income-estimation-at-the-heart-of-responsible-lending [to_ping] => [pinged] => [post_modified] => 2023-05-09 10:25:20 [post_modified_gmt] => 2023-05-09 09:25:20 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14508 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw ))[1] => Array ( [post] => WP_Post Object ( [ID] => 14174 [post_author] => 1 [post_date] => 2020-07-28 17:17:13 [post_date_gmt] => 2020-07-28 16:17:13 [post_content] => [post_title] => How Open Banking's arrival is removing consumer friction in credit application across Europe [post_excerpt] => [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => how-open-bankings-arrival-is-removing-consumer-friction-in-credit-application-across-europe [to_ping] => [pinged] => [post_modified] => 2020-08-26 14:42:13 [post_modified_gmt] => 2020-08-26 13:42:13 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14174 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw ))[2] => Array ( [post] => WP_Post Object ( [ID] => 14722 [post_author] => 1 [post_date] => 2021-10-21 12:58:28 [post_date_gmt] => 2021-10-21 11:58:28 [post_content] => asdjahksdhakj dh adskjha dsailoasjhduklasdh kajdBrightcove[cta_block] [post_title] => Covid-19 a look at the new normal - are we witnessing a structural change in the South African credit industry? [post_excerpt] => [post_status] => publish [comment_status] => closed [ping_status] => closed [post_password] => [post_name] => covid-19-a-look-at-the-new-normal-are-we-witnessing-a-structural-change-in-the-south-african-credit-industry-2 [to_ping] => [pinged] => [post_modified] => 2022-01-28 15:29:03 [post_modified_gmt] => 2022-01-28 15:29:03 [post_content_filtered] => [post_parent] => 0 [guid] => https://exp-lt.webjuicer.co.uk/?p=14722 [menu_order] => 0 [post_type] => post [post_mime_type] => [comment_count] => 0 [filter] => raw )))

Further reading

Income estimation at the heart of responsible lending

In today’s financial market, it’s critical to have a comprehensive view of your customers’ ability to pay in both the short and longer term. Read our blog for more insight.

How Open Banking’s arrival is removing consumer friction in credit application across Europe

TBC

Covid-19 a look at the new normal – are we witnessing a structural change in the South African credit industry?

EMEA Experian · Web Data Insights – Giulio Mariani asdjahksdhakj dh adskjha dsa iloasjhduklasdh kajd Brightcove

Vev as a post

Capturing the digital identity evolution through a layered approach

As digital adoption has increased, identities have become more complex. Read our whitepaper for insight into the future of digital identity.

Whitepaper functionality test – Andrew King

Meta description

The different types of fraud and how they’re changing

Fraud prevention in a Covid-19 environment

The current pandemic has meant that more consumers are now forced to access products and services online. Watch our webinar to discover how you can apply fraud prevention actions to protect your business and your customers.

A holistic approach for IFRS 9 Validation

TBC

Pandemic-driven ID theft trends in Europe

This webinar focuses on the post-pandemic, acute rise in identity theft throughout Europe, and what you can do to protect yourself and your clients.